Executive Summary

- Since the first payroll contractions began in early 2024, private sector employment has remained locked in a "no-hire, no-fire" pattern, failing to regain meaningful growth momentum.

- Benchmark revisions have materially altered the narrative, shifting previously reported strength into a position of caution.

- Part-time employment indicators show growing tension as employers opt for flexible hours over full-time commitments.

A common theme I often return to is that aggregated data series tend to send misleading signals. As I pointed out in my consumer credit report, spending and savings ratios are dominated by higher-income households. If the economy was as robust as GDP portrays, one would not expect to see a continual structural weakening in the labor market.

Part-Time for Economic Reasons Breaks Above 5 Million

The following charts show "part-time for economic reasons" and the rates of change between part-time and full-time employment. During recessions, part-time employment rises as full-time declines. Currently, part-time growth is outpacing full-time, indicating building stress.

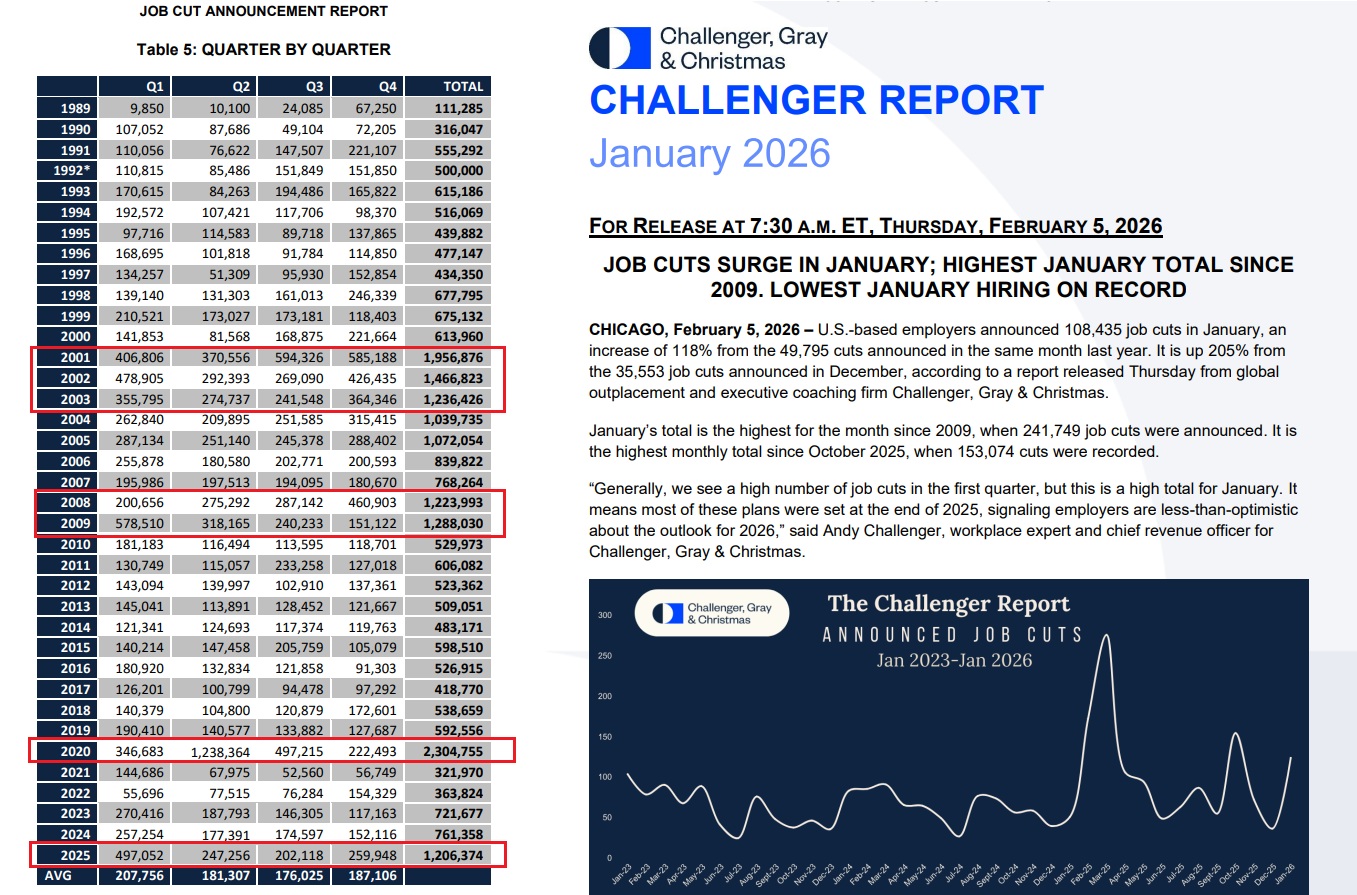

The "no hire, no fire" labor market is a phenomenon where employers are hesitant to both hire new talent and lay off existing staff. Some argue that the required employment rate for stability is now much lower due to immigration and demographic shifts. The following charts show the clear structural weakness seen visually — the first chart showing a breakout of the private sector (blue) and all employment (red). In the second chart, the composition of employment is telling of an economy being supported by non-cyclical [Cyclical vs Non-Cyclical →] employers (blue). Healthcare and Social Assistance represented 104% of all employment in 2025. Finally, Challenger, Gray & Christmas reported 1.2 million layoff announcements in 2025 — a level historically associated with recessions or the immediate aftermath of one.

Chaos Theory Outlook

It is possible we enter a shallow labor market recession in 2026 that doesn't push GDP negative, thanks to the sheer size of AI hyperscaler capital expenditure — estimated at $700 billion. The stock market, driven by this capex and the top-tier wealth effect, will further the "K"-shaped economy. I believe equity markets lead the economy.